Close

To commemorate the ICF’s International Coaching Week (16 May – 22 May 2022) and IIA’s Internal Audit Awareness Month (1st May – 31 May 2022), two fields I am passionate about, I am writing a short series of articles on the interpersonal and human aspects of internal audit and why I believe they are so important.

The theme of my first article in this series is “Psychological safety and freedom in internal audit”.

Internal audit can be a mentally and emotionally vulnerable experience for both the auditor and the auditee. The auditor is expected to enter the world of the auditee to understand, assess, challenge and report on an area or process in which they may not be the expert, yet have the authority to conduct this exercise. This can and may give rise to concerns such as being out of depth and missing out important aspects and these concerns may become a reality through the quality and direction of the dialogue with the auditee and later with the IA leadership.

Likewise, the auditee is likely to be equally apprehensive about the experience; not because they are not an authority on their process but because in spite of it, they may not have the ability to convince the auditor that how they have run their area is the best they could, given what they knew at the time, their skills and abilities, the resources available to them, and the circumstances at that time. When a gap is identified, depending on how the observation is presented and the quality of the discussion, they may feel compelled to defend their process rather than engage in collaborative solutioning.

Both situations are very real, and it is here that psychological safety and freedom are enormously important.

As part of my coach training, I was introduced to the marvelous work of Dr. Carl R Rogers, one of America’s most distinguished psychologists, who pioneered the concept of client centered therapy. In his countless research, one of the most significant hypotheses which he went on to prove is that if certain attitudinal conditions are present in a relationship, then the other person will discover within themselves the capacity to use that relationship for growth, change and personal development.

I believe that such attitudinal conditions can have a profound impact in internal audit relationships to foster creativity and collaboration in two settings.

Let me clarify the creative process in this context. It is the process through which innovative ideas, suggestions, thoughts emerge out of the uniqueness of the individual on one hand and the materials, events, people, and circumstances of their life on the other. In internal audit, this can be out of the box solutions, more accurate and honest identification of root causes, unique ways to use technology and more. This creative process can and will exist within the IA team and with the auditee/process owner if the conditions are right.

One of the most important attitudinal conditions Dr. Rogers referred to was psychological safety and freedom. A Google study (Google’s Project Aristotle) on what makes successful teams called out psychological safety as the number one factor. Does an individual feel safe to take risks and be vulnerable in front of another? How often does a team member feel they could share their disagreement with a test step without being perceived as being unaware? How often can an auditee share their genuine on-the-ground challenges without being perceived as making excuses?

Dr. Rogers further expanded psychological safety and freedom into the following conditions:

Psychological Safety

Psychological Freedom

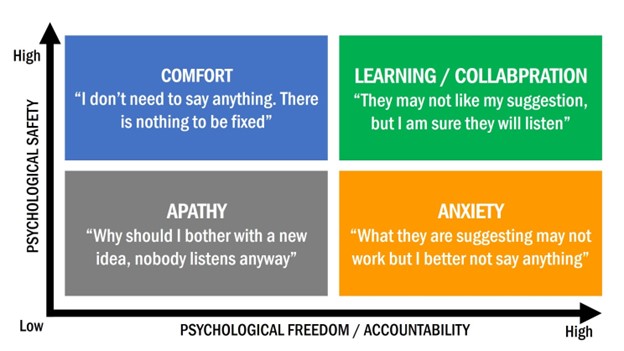

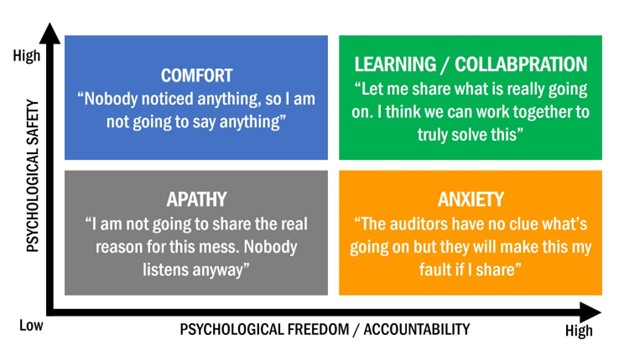

The chart below outlines what the outcomes may be depending on the psychological safety quotient at play in an internal audit relationship. (*Charts adapted from Google’s Project Oxygen results)

From the zone of the internal auditor

From the zone of the auditee / process owner

In an internal audit context, psychological safety and freedom starts with the acceptance that both the auditor and auditee genuinely want what is best for the organization with regards to risk management, controls and assurance and that, with the right psychological climate, they would genuinely share, engage and collaborate in finding the best outcome for the organization.

For such a climate to exist, leadership is critical. CAEs and audit managers should lead by example and take steps to create psychological safety for and within their teams and support and encourage them to create the same climate for their stakeholders.

The question each CAE should ask is how psychologically safe and free do their teams and stakeholders feel in an internal audit relationship? To make a shift towards increased safety and freedom requires deliberate actions on the part of the IA leadership through shifts in behaviors, new ways of working and raising the awareness of their teams on how to achieve this in their relationships with others.

In the face of the rapidly changing business, risk and regulatory landscape and increasing organizational expectations and change, professional coaching support has become an integral part of individual and team development for many organizations.

Likewise, professional coaching can have a tremendous impact on internal auditors in an individual and team capacity. Individual coaching is effective in raising awareness, drawing out personalized solutions and empowering action taking. Team-level coaching enables collective reflection and learning, helping the whole team improve their ways of working. A Deloitte paper on “Optimizing Internal Audit” highlighted that IA functions that have utilized coaches have seen significant increase in team performance and collaboration.

To find out more about professional coaching and power skills training for internal audit leaders and practitioners, please email me at info@bhavanijois.com